As approved by the Nitijela of the Marshall Islands, the normal retirement age is now fixed at 63 years.

Effective March 2017, MISSA has stopped granting early and deferred retirement benefits.

Pursuant to the Social Security Act, for workers who retired after March 6, 2017 and are under

65 years of age and are still working, their benefit amount shall be reduced by $1.00 for every

$3.00 earned in a quarter in excess of $1,500. This is called the Earnings Test (ET) application.

The adjustment in benefits will be applied as soon as practicable following the quarter in which

the earnings were made and reported. No adjustment is made for claimants who have attained the age of 65 years.

For those who retired prior to March 6, 2017, ET application was stopped at age 62.

Pursuant to Section 142 of the Social Security Act (the Act) found at 49 MIRC 142 (1) – Unless

modified by a totalization or bilateral agreement, no more than six (6) months of benefit

payments under this Chapter shall be paid to any beneficiary who is not a citizen or national of

the republic while the beneficiary has been outside of the republic; provided, however,

payments shall be made to citizens and nationals of the Federated States of Micronesia (FSM),

the republic of Palau (ROP), and the Unites States of America (USA) as if they were citizens or

nationals of the republic, if FSM, ROP and USA, respectively, extend reciprocal benefits to

citizens of the Marshall Islands.

For workers who retired prior to March 6, 2017, the maximum monthly benefit is $1,600, while

those who retired on March 6, 2017 or after, the maximum monthly benefit is capped at

$1,200.

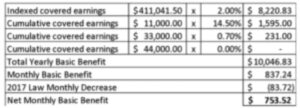

Retirement Benefits are computed on the Basic Benefit. The Basic Benefit is one-twelfth (1/12)

of the sum of the pension element and the social element, where the pension element is two

percent (2%) of indexed covered earnings and the social element is fourteen and one-half

percent (14.5%) of the first $11,000 of cumulative covered earnings plus seven-tenths percent

(0.7%) of cumulative covered earnings in excess of $11,000 but not in excess of $44,000.

Below is a sample calculation of basic benefit assuming that indexed covered earnings is $411,041.50:

No. Double dipping is not allowed. However, the surviving beneficiary will receive the benefit

with the higher amount.

- Death;

- If a medical retiree was able to recover from disability and finds gainful employment;

- If a surviving spouse has remarried (by legal or common-law marriage);

- If a surviving child who has reached the age of 18 has stopped going to school, or has

married or has found gainful employment; or if in school, has reached the age of 22.

No. Contributions are non-refundable, unless the wage earner has two or more employers in the Marshall Islands (on the same period) and his or her quarterly contributions exceeded the required amount. If the wage earner reaches the age of 60, he or she may apply for a lump sum payment computed at 4% of the total cumulative taxable wages.

Earned wages of an employee are computed based on actual payments by his or her employer. If, for example, out of the eighty quarters of contributions by the employee, fifty (50) quarters were not remitted to MISSA by the employer, then, only thirty (30) quarters of earned wages will be credited to the employee’s wage history. Thus, the employee can not retire, even if retirement age has already been attained.

Yes. The Marshall Islands has entered into a totalization agreement with Palau and FSM. This agreement enables any Marshallese, Palauan or FSM citizen who is not eligible for a monthly old-age retirement benefit under the social security administration of any of these countries but has worked and paid social security contributions to two or all of the three countries, to combine his or her credited service earned under two or all three systems and becomes eligible for benefits.

On November 2, 2018, P.L. 2018-98 was passed by the Nitijela, giving non-citizens the option to

receive lump-sum benefits equivalent to 80% of the workers’ contributions only but must meet

the age requirements under normal retirement and provided that such workers will return for

good to their own countries. Payment shall be made in two installments: 70% of the 80% shall be paid upon approval of the claim while the remaining 30% shall be withheld by MISSA for not

less than 90 days.